The policies (and lack thereof) that lead to bank crises

U-shaped monetary policy, Silicon Valley Bank, and the role of macroprudential policies in tomorrow's economy

In light of the recent failures of Silicon Valley Bank, Signature Bank, and First Republic Bank, let’s look at the monetary policy that preceded the banks failing. Furthermore, what can policy makers do to detect and reduce financial risks that arise throughout a business cycle?

A recent report from economists at the Barcelona School of Economics explains how U-shaped monetary policy increases the risk of banking crises. U-shaped monetary policy happens when the interest rate set by central banks literally forms a “U” on a graph. For example, the graph below shows the Federal Reserve rate path of the last four-ish years leading up to the recent bank failures:

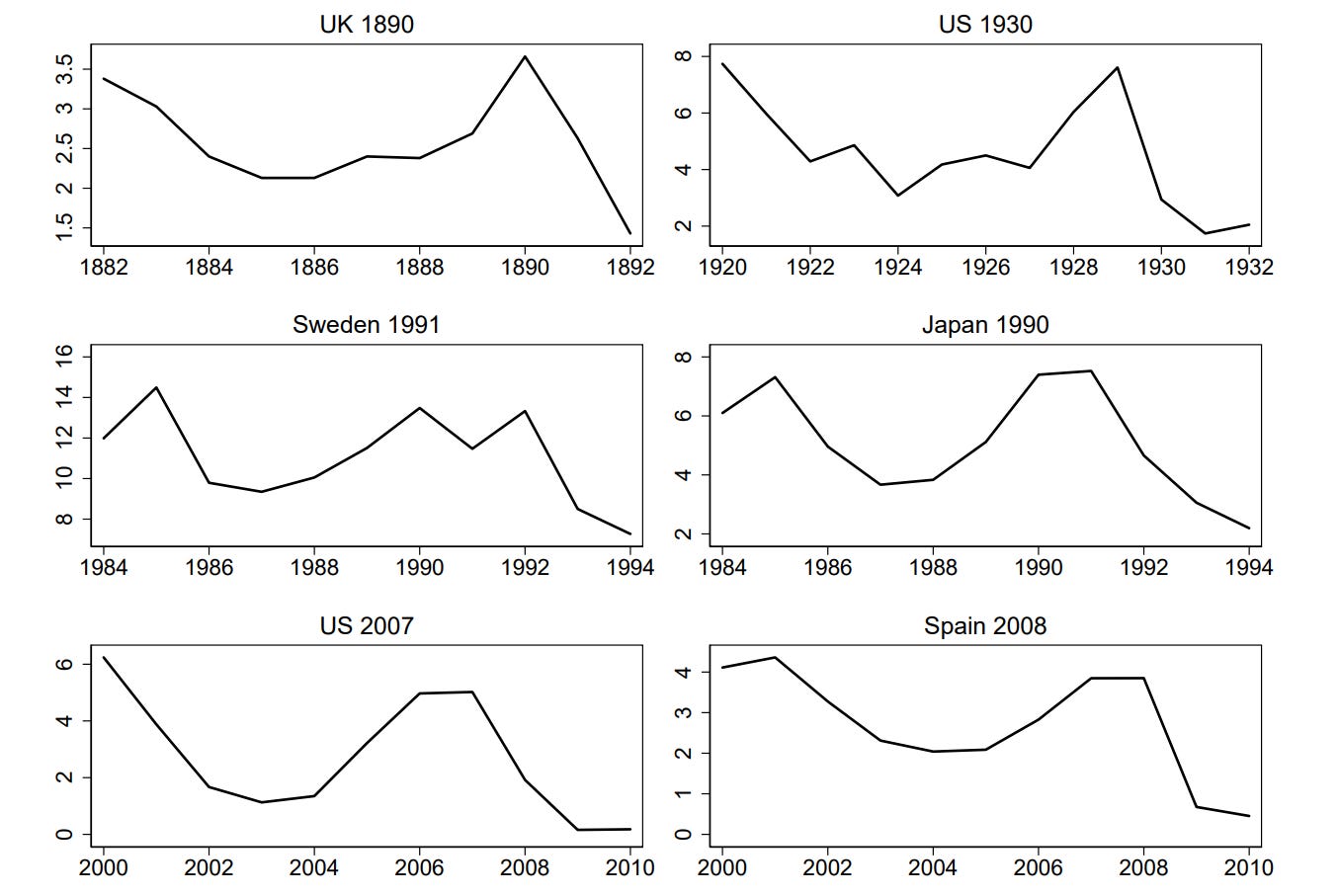

And below are similar rate paths that preceded bank failures of the past:

Jimenez et al, at BSE, explain the phenomenon as follows,

…the average crisis is preceded by U-shaped monetary policy, with a series of cuts in interest rates 7 to 4 years before the crisis followed by increases during the three years in the run-up to the crisis.

Schularick and Taylor (2012), define systemic banking crises as “events during which a country’s banking sector experiences bank runs, sharp increases in default rates accompanied by large losses of capital that result in public intervention, bankruptcy, or forced merger of financial institutions.”

It’s important to distinguish bank crises from recessions. A recession is usually defined as a sustained period of weak or negative GDP growth and high unemployment. Recessions don’t have to involve the financial sector. A bank crisis, on the other hand, is financial sector-specific.

Now, how do these economists know that the U-shaped rate path actually caused the banking crises? After all, correlation doesn’t always mean causation. The BSE economists used two strategies to identify the U-shaped rate path as a culprit.

First, they examined the relationship between banking crises and four common monetary policy rate shapes: cut-raise (U-shaped), raise-raise, raise-cut, and cut-cut. They found that U-shaped rate paths are the most common culprit across different levels of crisis and economic eras (pre and post-WW2), as seen in the graph below. Note that every single deep banking crisis after World War 2 was preceded by U-shaped monetary policy:

Next, the BSE economists used a regression framework to analyze crisis likelihood after differing rate paths. I won’t get into the weeds on how the regression works using trilemma instruments and crisis dummies, but the highlights of their results can be summarized from the following quotes:

…a sequence of reducing rates and then increasing them by 1 percentage point over three years is associated with a 12 percentage points increase in crisis risk, more than doubling the crisis probability…

…The longer a low interest rate environment has lasted, the higher the risk of triggering a crisis by increasing rates… [and]

…as monetary policy rates are cut over a long time period, credit and asset price booms and banking sector vulnerabilities build up. When monetary rates are subsequently raised, these financial vulnerabilities crystallize, with bank stock returns and profits decreasing, potentially triggering a banking crisis.

Ok. So U-shaped monetary policy rate paths lead to banking crises, but how exactly?

Banks are especially sensitive to the federal interest rates because so much of their business is selling (and buying) interest-rate-sensitive financial instruments. Let’s look at Silicon Valley Bank (SVB) as an example.

SVB bought a ton of government bonds back when interest rates were low in 2020-2021. When the Fed raised interest rates in response to high inflation, the government bonds decreased in value. In order to get their original money back, SVB would have needed to hold their bonds until maturity (which was still years away).

Meanwhile, SVB did not have any liquid investments that they could sell to pay interest to their depositors. They were insolvent, bleeding cash, and when their customers noticed, they all went to withdraw their deposits at the same time (a bank run). This bank run led to the US government taking control of the bank and saving us from further financial disaster.

In more technical terms, Jimenez et al found the following:

Consistently, we find that U-shaped monetary policy increases the probability of ex-post loan defaults, but effects are much stronger for ex-ante riskier firms (including real estate firms) and for banks with weaker balance sheets, especially lending to ex-ante riskier firms.

SVB was definitely a risky bank with a weak balance sheet. U-shaped monetary policy may have opened the door for SVB to fail, but it was ultimately SVB’s un-diversified investments/customers, and poor foresight that led to their demise.

So, how can we better prepare for U-shaped rate paths in the future? The BSE researchers conclude their paper by recommending, among other things, macroprudential policy.

Macroprudential policy can be used to reduce the unintended effects of monetary policy and gives monetary policymakers more room to achieve their goal of price stability. In other words - when we encounter scenarios where U-shaped policy is necessary to address price stability, we can decrease risks for banks by implementing macroprudential policy.

Macroprudential tools come in many shapes and sizes, and I plan to do a deeper dive into these types of policies in the future, but two common examples are policies that require banks to:

build a sort of “rainy-day fund” to buffer against interest rate risk

be more risk-averse by implementing debt-to-income requirements for mortgage borrowers

Basically, they’re policies that require financial institutions to be more risk-averse.

Macroprudential policy has gained in popularity since the 2008 financial crisis with regulating committees popping up in countries around the world. The US created the Financial Stability Oversight Council in 2010 with the same idea in mind. Unfortunately, the US’s Secretary of the Treasury-led council does not have enough authority to implement policies like the ones listed above.

So far, the council has not been able to implement any major macroprudential policies recommended by economists - especially countercyclical policies meant to reduce the aforementioned side effects of U-shaped monetary policy rate paths.

The US needs better governing tools, like macroprudential policy, to help protect the economy from risky financial sectors, and to protect risky financial sectors from themselves.

Monetary policy is a valuable tool that has some negative side-effects in certain scenarios, but better financial regulation can help us reduce the negative effects of the business cycle. For guidance, we should look to researchers that are uncovering the intricacies of U-shaped rate paths, and the benefits of macroprudential policies to keep our financial sector healthy during all rate path scenarios.